Inflation and Interest Rates

You are worried about it. You have heard that interest rates have been increased to fight it. Even as concepts like inflation and interest rates affect your lives daily, do you really understand what this all means?

EASY EXPLAINERS

Rasleen Sandhu

6/17/20246 min read

Part 1. Supply, Demand & Price

First, we need to understand supply and demand. Simply put, supply is the amount of stuff & services available to sell. On the other hand, demand is the amount of stuff & services that people want to and are able to buy. What's important to understand is that we look at demand and supply relative to each other. That's how prices are decided in the market.

Let's imagine a market with just three people -

In scenario 1, there are 2 chocolate sellers and 1 buyer. Both sellers have 1 chocolate each available to sell. So, supply = 2. But the buyer only wants to buy 1 chocolate. So, demand = 1. Think about who would have more power in that situation to affect the price of chocolate. The buyer would, because she can choose to buy any of the two chocolates but the sellers can only sell to her. Only 1 of the 2 chocolates would be bought. Thus, the two sellers compete to sell him their chocolate, likely with price. In this process, they would drop the price to make the sale.

So, if demand is lower than supply, prices fall.

In scenario 2, it's the opposite - there are 2 chocolate buyers and 1 seller. 1 There is only 1 chocolate available to buy (so, supply = 1) but want for 2 chocolates (that's demand = 2). Who holds more power now? The seller. As there is only 1 chocolate, the buyers are the ones competing to buy that chocolate. He can just sell the chocolate to whoever is willing to pay a higher price for it.

So, if demand is higher than supply, prices increase.

Part 2. So, why did high inflation occur after COVID?

Of course, the explanation we talked about is very simple, and real life is way more complicated. But the core concept about how prices work stays the same.

When COVID happened, it disrupted a lot of things -

Supply chain problems - People getting sick, lockdowns, and travel restrictions caused production and transportation of goods to slow down. That reduced the supply.

Plus, at the start of the pandemic, companies in many sectors laid off workers, which also reduced their ability to produce things.

During the lockdown, people were staying and home and spending less, which meant that they saved money. But when the lockdowns were lifted, people both wanted to buy more and had the money to do so. That increased the demand.

Thus, after lockdowns were lifted, demand increased but the supply did not.

Pandemic-related disruptions took time to solve but there were also more issues -

More disruptions like the wars in Ukraine and Gaza, affected the supply of important things like oil and grain.

As the companies tried to hire back workers after laying them off, there was more competition for workers in some sectors, resulting in higher wages. (This is supply and demand too - more demand for workers but less supply means, an increase in wages, or vice-versa). The companies would transfer these higher costs to customers by increasing prices.

Further, geopolitical tensions between China and the US caused them to raise tariffs (tax on import/export) on each other, increasing the price of goods.

Concerns about the fragile nature of the global supply chain and fears of political tension also caused some companies to reduce their dependence on China, where goods are produced cheaper. These disruptions also caused supply to decrease and costs of production to increase.

All of this caused prices to rise quickly, resulting in high inflation.

Part 4. Why did the Bank of Canada increase interest rates?

But first, what are interest rates, anyway? Simply put, it is the cost of borrowing. If you give a loan of $100 at an interest rate of, say, 4%, I will have to pay you back $100 + $4 in interest.

So, how do Central Banks determine how much everyone charges to borrow from each other? In the case of the Bank of Canada, it's by changing what's called an overnight interest rate.

Every day, Canada’s banks move money between each other for their customers - e.g. whenever you use your credit card or send an e-transfer. At the end of each day, they need to settle all these payments. Some institutions may have sent out more in payments than they received, while others may have received more than they sent. To balance out the payments, financial institutions can borrow money from each other for one day.

In addition, they can also borrow from the Bank of Canada. The Bank of Canada decides on what interest rate to charge them. That impacts what interest they charge each other, businesses, and households. That eventually affects how much interest rate everyone pays.

Now back to how interest rates are related to inflation -

If inflation is caused by a gap between (higher) demand and (lower) supply. Then, there are 2 ways to try to reduce inflation - Decrease demand or increase supply. Increasing the supply of goods is a complicated, difficult process that takes time and the Bank of Canada does not have the tools to do so.

Instead, they try to decrease demand in the market. This is where interest rates come in.

As we discussed before, interest rates determine the cost of borrowing money. Increasing interest rates make it more expensive and difficult to borrow money to buy a house, a car, or expand a business. Homeowners also have to pay higher mortgage rates, leaving them less money to spend on other things. In essence, higher interest rates discourage households and businesses from spending money and thus, reduce demand.

In addition, as interest rates increase, saving becomes more attractive as people can get higher rates of interest from banks.

Another reason that it increases interest rates is to prevent the 'wage spiral'. Higher inflation can cause people to expect more inflation in the future, causing them to ask for an increase in wages, which can cause businesses to raise their prices to accommodate for wage increases. This can turn into a cycle of ever-increasing inflation. This is counteracted by decreasing the spending ability of businesses and sending the message that inflation will get under control. (Please note that the concept and existence of the 'wage spiral' is heavily debated by economists).

At least theoretically, this is how it is supposed to work. However, there are risks and harms associated with increasing interest rates to control inflation-

The process itself is quite painful for households and businesses. The combination of high prices and high interest rates significantly decreases their purchasing power and can severely hurt their financial well-being.

There is a lag in changing interest rates and when their impact can be seen. So, there is a risk that increasing interest rates will decrease demand too much and cause a depression.

Increasing interest rates can also hurt businesses' ability to pay their employees, causing layoffs and thus, increasing unemployment.

There are some questions about the effectiveness of fighting inflation by increasing interest rates to decrease demand when the problem is caused by supply-side issues.

Further, there are debates about the complex inflationary effects of high interest rates themselves, e.g. how much do higher mortgage rates themselves contribute to inflation.

Therefore, making such decisions is about carefully monitoring, analyzing, and assessing how much and when to increase interest rates + comparing the benefits and risks of such measures.

Part 3. Inflation, purchasing power, and why a little inflation might be good, actually?

Inflation refers to the rate at which the general level of prices for goods and services rises, as a percentage over time.

Another concept that will become important later is purchasing power -

Purchasing power refers to the amount of products and services you can buy with a currency. As prices of goods rise, the amount of stuff you can buy with the same amount of money decreases. Goods become more expensive, but $100 stays $100, so the purchasing power has decreased. That's why the same $100 is considered of less value today than it was 100 years ago.

Here, I want to make something very clear. Rising prices are not the problem. In fact, most economists believe that a little inflation is actually good. To be precise, central banks usually want an inflation rate between 1% to 3%.

This is because of a few reasons -

As people expect things to get more expensive over time and the purchasing power of money decreases, people buy more things now rather than later. Thus, people are incentivized to spend or invest their money rather than just save it. This helps boost the economy.

If the inflation rate is maintained around 2%, it provides a cushion against fluctuation in prices and reduces the risk of deflation (fall in prices), which is arguably worse.

Further, it gives the central banks the ability to boost the economy during a downturn by lowering interest rates (I'll explain that in the next part)

So, as long as wages rise alongside it, a slow and steady rise in prices won't hurt people. The problem happens when there is a high inflation rate. That means the prices rise too fast and unpredictably for wages to keep up. The increased cost of living very quickly reduces the purchasing power of money as well as value of people's savings.

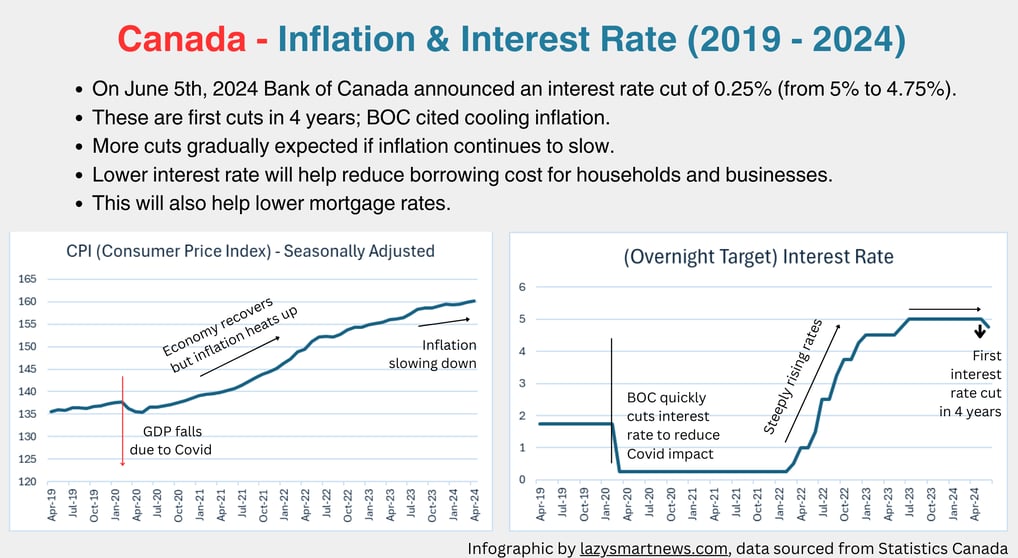

For now, at least there is some good news, Bank of Canada is the first among G7 countries to cut interest rates. The cut is only .25% but it is a good indication for the future.

Want us to easy explain something?

Let us know and we will be happy to.